Security industry economic outlook: cautious optimism

With the start of a new year, the early indicators reveal a security industry that appears to be in good health and promising solid growth after shedding the weight of the pandemic and supply chain problems in the last few years.

Integrators and consultants are feeling optimistic about their business and growth prospects. But they are keeping a watchful eye on external factors they can’t control – chiefly the presidential election in November, as well as global conflicts, supply chain disruptions and the break–neck pace of technology innovation.

SecurityInfoWatch scoured through leading reports from the industry – including its own State of the Industry Report – and interviewed executives in the integrator market to gauge what 2024 could look like.

Foundation of Growth

Security Business’ State of the Industry report is a comprehensive research survey of the industry’s top security systems integrators and consultants. The report assesses the state of the business in the security services marketplace.

The majority of companies participating in the report saw a rebound in sales and profits last year despite unprecedented supply chain and economic issues that continue to shape the business landscape.

The security and fire integration markets have become an attractive option for private equity, which continues to expand into the industry via acquisition.

Technological expansions into subscription services and artificial intelligence have become dynamic avenues for integrator growth and customer satisfaction.

About 75% of integrators and consultants said gross revenue was up slightly or significantly in 2023 over the prior year and 16% said it was about even. It was a similar story with gross profit margins, with 67% reporting they were up slightly significantly and 16% again saying margins were even.

As the industry continues to transition to an RMR model, 68% of respondents said that was “up significantly or slightly” over 2022, and 23% said it was even.

About 65% of respondents said the volume of security projects was up in the past six months in 2023 vs. 2022, with 25% saying it was even. And roughly 60% of respondents said project backlogs were up “slightly or significantly,” and only 15% indicated a downturn.

More than half of Integrators and consultants said economic factors like fuel costs, inflation and interest rate hikes, increased employee wages or undercutting and competition on price were their biggest threat to margins.

Some 70% said product shortages were still an issue but had had dissipated since 2022. They took a variety of steps, including shifting to new manufacturing partners, increasing internal stock, raising prices or working with new distributors.

Almost six in 10 respondents said they’ve been approached about selling their business in the last 18 months, with roughly the same percentage of private equity firms as another integrator or alarm company.

When asked about their top-performing verticals, corporate and smart buildings, industrial markets, education and critical infrastructure were the biggest leaders.

The Security Industry Association’s Security Market Index, conducted shortly before the ISC East show last November, was also optimistic about the physical security industry going into 2024.

The November-December Security Market Index noted a slight downward trend to 54 from September-October’s 59, but still met its average of 56 over a 12-month period. Growth for the security industry is indicated by any reading over 50.

The majority of the survey’s respondents (85%) reported “excellent” or “good” conditions for their companies, with 11% categorizing them as “average” and 4% as “fair”. None of those surveyed believed their companies were in “poor” economic condition.

Though some expressed some overall concern with economic confidence, others noted the security industry is different: “It’s crazy times for most, but wars, weather, protests and such drive our business.”

Participants remained optimistic regarding economic improvement for their businesses, with two-thirds reporting a belief that things will get “much better” (18%) or a “little better” (46%). About 29% predicted no change in conditions, and 6% expected conditions to get a “little worse.”

While the outlook is largely positive, concerns about economic recession, geopolitical conflicts, a tense upcoming presidential election, and Congressional budget impasses caused a slight dip in these numbers as compared to the previous survey’s findings.

When asked what was projected for their business in 2024, 61% of participants predicted growth of 5% or more. Only 8% of participants said their business would retain the same level of growth from 2023.

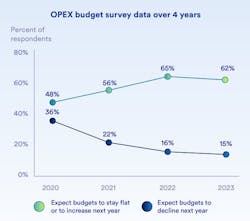

Genetec’s State of Physical Security Industry study found a majority of end users expecting increased OPEX budgets in both 2022 and 2023. About 62% of end users reported they expect to maintain or increase their OPEX budgets going into 2024, with only 15% of respondents expecting lower budgets.

Additionally, the market for video surveillance equipment saw a positive surge, with a 19% growth in the Americas and 12% in Europe/Middle East/Africa, as reported by Novaira Insights in 2022.

Executives interviewed by SecurityInfoWatch painted an optimistic economic picture for the industry this year.

“We are expecting 18-20 % growth in 2024. Our leading indicators are larger-than-ever backlogs, and the supply challenges are behind us,” says John Nemerofsky, Chief Operating Officer at SAGE Integration. “The other factor is that the projects our clients have forecasted are funded and have a 2024 deadline for completion. Most of this is being driven by workplace safety.

Pierre Bourgeix, CEO and founder of ESI Convergint, says he believes -- as he did 10 years ago -- that the security industry will continue seeing greater consolidation.

“Although I feel optimistic, I have reservations on how effectively some of our existing technology will survive past the quantum bubble,” he says. “The next decade will see greater cloud enablement and more powerful, faster and flexible compute, which will create a paradoxical bubble created by the growth of super computing and quantum-level processing.”

Bourgeix believes technology throughout could fall victim to that trend without adequate preparation to adapt to the change.

“Bubbles" tend to create change, he adds, and inevitably burst – “leaving many to be sidelined due to their lack of innovation and investment. Consolidation will become the answer to some of the security industries challenges and lead to external innovators that will introduce technology that will harness cloud and compute and generate a group of new leaders,” he adds.

“Those who are already on their way will be the first to celebrate the next 10 years of fast-paced growth in the industry.”

With the benefits of artificial intelligence, machine learning and robotics, the physical security industry promises to be robust in 2024, says John Slotnick, President of Setracon.

High levels of data integrations, including information streams from physical security devices, building management systems, publicly available records and data services that are imagined by humans and managed by AI and machine learning, “will add great perspective to the physical security industry and assist us in taking a proactive approach to risks,” Slotnick says.

March of the Disruptors

SecurityInfoWatch asked integrators and consultants what technology disruptors are poised to impact innovation and product development that could lead to new markets being opened in 2024.

Nemerofsky says it’s the deployment of AI solutions to solve client-specific problems in both access control and surveillance. “The other disruptor,” he says, “will be the demand for both manufacturers and integrators to be SOC2 compliant as regulated by the AICPA.”

Bourgeix says the security industry will continue to use deep learning and machine learning to develop generative AI, which will spur on greater innovation in technology that will adapt in a multitude of ways – leading to new markets being developed.

“This also will lead to greater uses of current security technology such as cameras, access control, sensors and the like to help the operational- and business-infrastructure world,” Bourgeix says. “These advances will breed innovation that is multidimensional and focused on greater outcomes beyond threats and vulnerabilities in our traditional security environment. The disruptors will continue to come from outside the security industry and adapt advancements to find new ways to solve today's problems.”

Slotnick asserts that robotics, and not necessarily humanoid-form robots, are slowly gaining acceptance as an augmentation to human security services.

“Robotics never sleep, do not need time off, have no human resource issues, and provide highly intelligent services, allowing the repurposing of human beings to more discerning and intelligent tasks,” Slotnick explains. “Integrating robotics into physical security is a great cost-effective answer to the ‘Great Resignation.’”

Eyes on Geopolitical Conflict, Election

Despite the general optimism in the industry, stakeholders are certainly concerned about the presidential election this fall and the potential fallout on economic and regulatory policy.

Nearly 60% of respondents said the 2024 presidential election is the top geopolitical issue that will impact security business moving forward. A distant second was U.S./China trade relations, and global conflicts like Russia-Ukraine and Israel-Hamas were also distant concerns.

“I strongly believe as an industry we have become much better at planning and forecasting. Our clients have made their projection for 2024 and as integrators we have forecasted to our key suppliers and distributors to plan for 2024,” Nemerofsky says.

Bourgeix says the ebb and flow of global conflict will spur on new advancements, especially in the “.gov” space and military arena, which tends to create leaps in technological advancements born out of necessity.

“Although the conflicts have created some short-term supply chain restraints, I believe this will change in the third quarter. Adjustments made through sourcing and distribution will help ease the restraints that are presently felt. Also, as we move to more software and cloud-based technology, we will see a lessening of issues occurring due to regional conflicts.”

“We have been speaking about public-private partnerships for many years. And in many cases, these partnerships have proven their value,” notes Slotnick. “Most critical infrastructure is privately owned. Many countries and governments require the goods and services provided by the private sector, so there is a beneficial and symbiotic relationship.

“Global corporations must address these risks to stay competitive in their respective industries. Governments are responsible for ensuring the safety and security of international shipping lanes and areas of instability. Because the same threat actors’ impact both groups, I foresee greater collaboration for mutual benefit.”

Mixed Indicators for Economy

Though fears of an economic recession remain high, economic indicators are trending toward the positive. According to the Bureau of Economic Analysis, the third quarter saw the gross domestic product (GDP) increase by 4.9%, more than double its 2.1% expansion in the previous three months. Unemployment rose to 3.9% despite the economy adding over 150,000 jobs in October, though it has remained under 4% since March 2022.

The Bureau of Labor Statistics reported that inflation rose in December, but markets were still expecting a rate cut from the by the Federal Reserve. Consumer confidence, after declining for three consecutive months, showed a postive rebound in the most recent report from the Conference Board’s Consumer Index.

The Dodge Construction network (DCN) expects conditions for residential and nonresidential construction to begin improving, placing them in a better position for growth. The Fed's indication of possibly cutting interest rates will be a major departure from its past decisions to hold rates steady.

While the odds favor growth, three new risks have been added to a long list of concerns: the rising probability of an extended federal government shutdown, possible new union strikes and higher energy prices created by the conflict between Israel and Hamas, the report says.

Each is expected to negatively affect the economy on a small scale at the very least but also carry the risk of a more serious impact. The Israeli-Hamas war, for example, is expected to bring West Texas crude prices to a peak of $85/bbl in the first quarter of 2024 before easing back to $77/bbl by the final quarter. If oil prices rise above the psychological threshold of $100/barrel for an extended period, however, the economy could slip into a recession.

In Washington, D.C., the new Speaker of the House, Mike Johnson, may not be willing or able to forge agreements across party lines. That would significantly raise the specter of a federal government shutdown.

The most likely result is a limited, two-week government shutdown but with a distinct possibility it could last longer. While the UAW strike ended, it hurt GDP growth. Since then, unions in other sectors have considered strikes to forge better wages for their members.

Construction outlook favors growth for security integrators

In general, the outlook for construction this year is favorable, which means there should be a steady supply of work for integrators and consultants. Stakeholders made similar comments about an increased volume of work in the Security Business State of the Industry report.

The Dodge Construction Network (DCN) Outlook for 2024 predicts total construction starts will rise in 2024. Overall construction starts are expected to rise 7% in 2024, following a 1% increase in 2023, said Richard Branch, chief economist at DCN, said during the 2024 DCN Construction Outlook.

The 2023 increase will bring total starts to an estimated $1.124 trillion, with $1.2 trillion forecast for 2024.

In the residential sector, Dodge predicts single-family construction would end 2023 down 12%, measured in units, before climbing 3% in 2024.

Branch notes that while the bottom for single-family starts has passed, mortgage rates need to ease before the sector will see stronger growth. Multi-family work is expected to follow a similar pattern, dropping 13% by the end of 2023, with a 3% increase in 2024.

The dollar value of starts in the commercial sector, which includes stores, offices, warehouses, hotels and parking, was expected to fall 6% to $156 billion in 2023, then another 2% to approximately $153 billion for 2024.

Branch attributes this due to warehouse construction, which was previously strong due to the rising popularity of online shopping, entering a cooling-off period. “I hesitate to call this an economic downturn,” Branch said, but a “recalibration” necessary after “one player [steps] out.”

After an astounding 217% increase in 2022, Dodge predicted manufacturing would fall slightly by the end of 2023 before increasing 16% in 2024.

The increase is “not a surprise, considering the impact of the CHIP and Inflation Reduction Acts,” said Branch.

Non-building starts, still bolstered by the Infrastructure Investment and Jobs Act (IIJA), were up 25% in 2023 and expected to increase an additional 7% in 2024. In the transportation sector, both bridge and street construction starts are forecast to end this year up 14%. In 2024, the value of bridge projects is predicted to rise 25%, with street construction not far behind with a 23% increase.

Don’t miss our State of the Industry webinar

Get more insight and analysis of Security Business’ State of the Industry report later this month by attending an exclusive webinar hosted by SecurityInfoWatch. The Jan. 31 event will feature a panel discussion with two seasoned experts who will speak about the business impact of many of the biggest industry trends and technologies. Click here to see the speakers and register.

About the Author

Samantha Schober

Associate Editor/SecurityInfoWatch.com

John Dobberstein

Managing Editor/SecurityInfoWatch.com

John Dobberstein is managing editor of SecurityInfoWatch.com and oversees all content creation for the website. Dobberstein continues a 34-year decorated journalism career that has included stops at a variety of newspapers and B2B magazines. He most recently served as senior editor for the Endeavor Business Media magazine Utility Products.