Key Highlights

- Security M&A driven by strategic forces, not just interest rates: Valuation gaps, tariff volatility, and technology capability needs shape 2026 deals more than Fed cuts, as manufacturers shift from service roll-ups to product/software acquisitions, PE investment cycles signal integrator platform turnover, and residential markets remain fragmented.

- Technology M&A replaces service consolidation playbook: After five years of integrator roll-ups, manufacturers now use acquisitions to backfill capability gaps—software/cloud architectures drive buyers like Motorola, Axon, and Honeywell ($5B on access control) toward "buy vs. build" strategies.

- Integration middle market changes: Growing customer demands, expanding security requirements, and organic growth redefine market scale—while PE capital accelerates consolidation, substantial room remains for next-tier players to build lucrative platforms in a less saturated segment than fire/life safety.

- PE five-year cycles trigger platform turnover wave: Vintage investments approaching exits will repurpose capital as PE seeks 3x returns; integrator platforms changing hands while residential stays fragmented (ADT 25%, SimpliSafe 5%, leaving 70% of $35-40B across thousands of players).

This article originally appeared in the January 2026 issue of Security Business magazine. Don’t forget to mention Security Business magazine on LinkedIn or our other social handles if you share it.

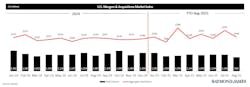

As the security industry enters 2026, business owners and executives are watching the mergers and acquisitions landscape with keen interest. With interest rate cuts underway and market dynamics shifting, many are anticipating a surge in deal activity.

To understand what’s really driving M&A in the security sector, Security Business caught up with Alper Cetingok, global head of the diversified industrial practice and co-head of the security & safety sector team for Raymond James, one of the industry’s most active investment banking advisors. What emerges from the conversation is a nuanced picture that challenges conventional assumptions while revealing deeper forces reshaping the competitive landscape across product manufacturers, service providers, and integration firms.

The security industry’s fundamentals remain favorable – security requirements are expanding, technology architectures are evolving, and customer demands are growing and becoming more sophisticated. These trends point to organic growth opportunities, but they also support sustained M&A activity across the sector.

Private equity capital will continue flowing in, creating both platform opportunities and tuck-in acquisition prospects. Manufacturers and technology vendors will increasingly use M&A to address capability gaps, potentially reshaping supply relationships and enhancing their ability to meet more of their customers’ needs. In the end, the M&A landscape in 2026 and beyond will be shaped by strategic forces like the imperative to acquire technology capabilities, the maturation of private equity investment cycles, and the ongoing evolution of customer demands across commercial and residential markets.

The Catalysts for M&A in 2026

Conventional wisdom in the security industry suggests that recent Federal Reserve interest rate cuts will trigger an avalanche of M&A activity; however, Cetingok offers a more measured perspective that should recalibrate expectations.

“I think generally speaking, that’s a fair assumption,” Cetingok acknowledges, but he points out that M&A in the security space has been very active for years, regardless of the interest rate environment. “It has been outsized relative to other [industries], so I don’t think rate cuts are going to have a material impact on our industry as it relates to the sheer volume of activity.”

He explains that the reality is that the key constraint on M&A isn’t the availability of financing; the primary friction point lies in the gap between buyer and seller expectations on valuation. “What will change the dynamic of the marketplace is either valuation levels going back up to what sellers are hoping to get or sellers capitulating to where buyers are willing to transact – and it is probably more the latter than the former,” Cetingok says.

More importantly, he notes that the historic M&A volumes were driven by essentially zero interest rates – a condition that will not return. “We’re not getting back to zero,” he says. “We’re going to come down incrementally, and every bit helps, for sure.”

If interest rates aren’t the primary catalyst, what is shaping M&A sentiment? Cetingok points to broader macroeconomic and psychological factors that loom larger in boardroom discussions. “It is much more related to the overall sentiment in the marketplace,” he explains. “Tariffs and other macroeconomic concerns are bigger impacts on the psychology of the M&A market today.”

The tariff question deserves particular attention, given its prominence in 2025 and 2026 business planning discussions. Initially, the uncertainty around tariffs created anxiety in deal negotiations; today, the market has adapted to what Cetingok characterizes as a “new world order” of trade policy volatility.

“I think people are less concerned about the next headline around tariffs, but there is a fundamental impact on business, for sure, and you have to price it in,” he explains. “Deals getting done today have some degree of pricing that accounts for tariff volatility. As tariffs are effectively used as a political weapon, they have to be accounted for in your business.”

A Technology Shift in M&A

For integrators watching manufacturing and technology partners, a significant trend is emerging that will reshape the competitive landscape. After years of service-heavy M&A activity in the security space, the pendulum is swinging toward product and technology acquisitions.

“If you look at the last five years as a measuring period, [M&A] has been heavily skewed to services – like integrator roll-ups or fire and life safety services roll-ups,” Cetingok observes. “It is still over-indexed to services, but we are seeing a lot more technology, hardware, and software-related transactions in the pipeline.”

This shift reflects fundamental changes in how the industry approaches innovation. Rather than relying solely on internal R&D, companies are increasingly using M&A as a strategic tool to address capability gaps. “Part of that is just the evolutionary curve in technology and product that has steepened in this industry over the course of the last five years,” Cetingok says.

“M&A is being used as a way to effectively backfill technology development gaps, and I think that’s going to continue,” he says, adding that the increasing role of software in the security space – driven mostly by cloud computing and architecture – will lead to M&A activity specifically in the software space.

Technology Acquirers: Familiar Faces and New Players

The question of who will be driving this technology-focused M&A wave brings both familiar names and some surprises. The established players remain committed to acquisition-driven growth strategies.

“I don’t see material changes in the acquirer landscape,” Cetingok says. “I think the ones who’ve been there – Motorola being a great example – are going to continue to do that. They’ve proven that M&A is a core component of their growth strategy, and their market value allows them a lot of latitude with which to be aggressive from an M&A perspective.”

But the more interesting development for Cetingok is the emergence of newer players who are beginning to flex their acquisition muscles. “Axon is a great example, and Flock has done some acquisitions as well to fill in parts of their portfolio,” he says. “And five years ago, you probably wouldn’t have predicted that Honeywell was going to spend $5 billion on an access control investment.”

This expansion of the acquirer base reflects a broader strategic reckoning among larger technology companies. “We are going to see bigger players really thinking critically about their portfolios, and not always in ‘buy mode,’” Cetingok says. “Johnson Controls is a great example in terms of what they’re doing with their [European and Latin American] ADT assets.”

The driving force behind this heightened M&A activity among larger players is straightforward: they have strong businesses, healthy balance sheets, and a realistic assessment of their own limitations. “The larger acquirers are really coming into the market more aggressively, going for buy vs. build,” Cetingok explains.

Monitoring Market: Emerging Consolidation

While alarm monitoring might seem like a mature, even declining sector, Cetingok sees a different picture emerging – one that suggests significant opportunity for consolidation. “I don’t think the market is shrinking; in fact, it is growing because there are more use-cases for monitoring than there have ever been,” he says.

The expansion of monitoring applications beyond traditional intrusion alarm to video verification, access control, and various managed services models is creating new growth vectors; however, the market structure has constrained M&A activity to date, perhaps due to a lack of multiple serial acquirers as seen in the integration, fire, or security technology markets.

“Other than Becklar, which is private equity-backed, there isn’t a natural consolidator in that market, which is part of the reason why you don’t see as much activity,” Cetingok explains, while noting that it may be changing. “As these businesses continue to grow and mature, more outside capital will come into that space. I personally know of probably 10 to 15 private equity funds that have done a deep dive around the monitoring market,” he reveals.

Redefining the Integrator Middle Market

For the security integration community, understanding the current M&A landscape requires recalibrating assumptions about market structure. The concern that middle-market integrators have been “gobbled up” by PE-backed platforms such as Sciens, Pavion, and others requires a more nuanced examination.

“I think the definition of middle market is changing,” Cetingok says. “The industry is growing, and you are seeing more and more players.”

As revealed in the Security Business State of the Industry report last month, the fundamental tailwinds driving integrator growth are stronger than ever. Customer demand is expanding, security requirements are increasing, and changing threat landscapes require more sophisticated solutions.

“There’s a lot of changing technology today, and customers are asking integrators to do a lot more,” Cetingok says. “[Integrators] need to come in and effectively enhance existing systems to adapt to a changing risk environment. Even the local integrator is benefiting from some portion of those trends – just maybe not in the same way or at the same magnitude. But that just means businesses are growing.”

[Integrators] need to come in and effectively enhance existing systems to adapt to a changing risk environment. Even the local integrator is benefiting from some portion of those trends – just maybe not in the same way or at the same magnitude. But that just means businesses are growing.

- Alper Cetingok, Raymond James

To illustrate the evolution of the integration channel, Cetingok harkens back to Allied Universal’s 2019 acquisition of Securadyne Systems. “[Securadyne] had about $75 million of revenue, which at the time, made it a top-10 integrator,” he says. “To be in the top 10 today, you have to be far larger than $75 million.”

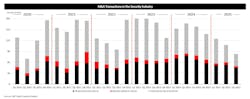

A large amount of that growth has come about organically; however, the influx of private equity capital and the focus on market consolidation have accelerated the shift in scale. Cetingok says that all of these factors, coupled with companies building enhanced service capabilities and focusing on geographic dispersion, have “been very additive to the M&A profile of the integrator community, and that’s going to continue for sure.” In fact, Cetingok believes that the security integration segment of the market is more fertile ground for private equity investment today than even fire & life safety because, “there are already approximately 40 private equity-backed fire & life safety companies, whereas sponsor-owned businesses in the integrator segment are at a fraction of that,” he notes.

“The integrator marketplace certainly has some large players – the JCIs of the world – but there’s still a lot of room for that next tier of player in that market,” Cetingok adds. “And there are lots of investors who believe that creating the next tier of player in that market could be very lucrative. Look at businesses like NextGen, Security 101, Minuteman – they are building into that next tier of players in the market, and from an execution standpoint, they’re doing a good job of getting there.”

Current PE Cycle Suggests Activity Ahead

For integrators owned by or partnered with private equity-backed platforms, understanding the investment cycle timeline provides important context for anticipating future market moves.

As Cetingok explains, the conventional playbook in private equity is plus or minus five years of investment. “You can use that as a benchmark – look at the date [PE] invested and go plus five,” he says. “Some take longer, some take shorter, but we are going to see a repurposing of that capital.”

This suggests significant turnover activity ahead. “If you just look at the vintages of the [PE] investments, the next several years would suggest we are going to see a lot of M&A activity in the integrator space,” Cetingok says. “These private equity-held businesses are going to turn over to new owners, and I think absolutely other private equity groups are going to buy. There’s a high degree of interest and demand.”

The trigger point for these transactions comes down to return thresholds. “The tipping point of value is really based on the entry valuation of that investor and that investor’s desired return on invested capital. For most private equity groups, that’s at least three times their money,” Cetingok explains.

Fragmentation Persists in Residential

The residential alarm company sector presents a markedly different consolidation story. Recent high-profile transactions, including GTCR’s acquisition of SimpliSafe, which is a transaction on which Cetingok advised on behalf of SimpliSafe and its private-equity backer Hellman & Friedman, might suggest a rush toward a consolidated market dominated by one or two players.

Cetingok pushes back on this narrative. “There is still [a large number] of players, and that local provider remains a really important part of the ecosystem,” he says.

If ADT has a 25% market share, and Simplisafe has around 5%, that means the remaining 70% of a $35-40 billion domestic market represents a substantial opportunity for thousands of companies. “That’s a lot of revenue opportunity for a lot of players,” Cetingok says. “Thousands of companies make up that 70%, so the structural makeup will not be shifting anytime soon.”

This means that while ADT remains at the top of the market, new entrants have established significant positions. “Simplisafe and Amazon Ring have built formidable businesses in the DIY segment of the market, and they are going to continue gaining market share,” Cetingok says. “However, you still have players like Vivint, Brinks, and the super regionals, like Alert 360 and CPI, so I believe that the market will remain quite fragmented for the foreseeable future.”

Editor’s note: Learn more about Alper Cetingok and Raymond James’s security industry services at www.raymondjames.com/corporations-and-institutions/investment-banking/industries-of-focus/diversified-industrials/security-and-safety.

About the Author

Paul Rothman

Editor-in-Chief/Security Business

Paul Rothman is Editor-in-Chief of Security Business magazine (www.securitybusinessmag.com) and has been covering the security industry for various outlets since 2001. Email him your comments and questions at [email protected].