Alarm Industry Players Overcoming Headwinds

The Skinny

-

Industry fundamentals remain strong: The U.S. security alarm industry has grown to $78B with steady 6–7% annual growth projected for 2025, fueled by specialty segments like video surveillance, smart home, and commercial projects.

-

Key challenges and strategies: Inflation, rising RMR creation costs, and margin pressures demand disciplined pricing strategies — with consistent 3–4% annual price increases proving both feasible and necessary.

-

M&A and consolidation: While smaller players still hold ~25% market share with strong retention advantages, consolidation continues, and valuations remain robust — favoring companies with strong reporting, metrics, and operational sophistication.

This article originally appeared in the August 2025 issue of Security Business magazine. Feel free to share, and please don’t forget to mention Security Business magazine on LinkedIn.

Industry overviews from expert analyst and dealmaker Michael Barnes of Barnes Associates have long been a staple of alarm industry events like the Electronic Security Expo (ESX), and this year was no exception, as Mr. Barnes delivered a fascinating look at the future of the security and alarm industries as part of his closing keynote in Cobb County, Ga.

Barnes thinks the electronic security industry stands at a pivotal moment in 2025, with fundamental shifts reshaping how companies compete, grow, and create value. His analysis focused on several critical, emerging trends that may very well define success for security integrators and alarm companies in the years ahead.

Here’s an overview of Mr. Barnes’s presentation at ESX. All numbers and figures come directly from his slide deck and/or his speech at the show. Feel free to visit www.barnesassociates.com to reach Mr. Barnes and his staff with follow-ups and questions.

Industry Growth: Strong Fundamentals with Evolving Dynamics

The US security alarm integrator market has evolved into a substantial $78 billion industry, representing remarkable growth from $37 billion just 20 years ago. The industry has maintained a healthy 5-6% annual growth rate coming out of COVID, with projections suggesting acceleration toward 6-7% growth in 2025. This consistency reflects the industry’s defensive characteristics, particularly evident during economic downturns.

This growth trajectory demonstrates the industry’s resilience and fundamental strength, with revenues roughly split between $41 billion in sales and installation revenue and $37 billion in recurring and related revenue streams.

While traditional residential and small-to-medium business intrusion and fire systems are growing at only around 3%, specialty segments are propelling overall industry expansion. According to Barnes, video surveillance leads this charge with 16%-plus growth that continues accelerating. The large commercial project segment is experiencing 11% growth, smart home solutions are maintaining 13% growth, and Personal Emergency Response Systems (PERS) and DIY segments are also continuing to expand.

Barnes explained that this shift toward specialty segments represents both opportunities and challenges. Companies must evaluate where they want to compete and adjust growth expectations accordingly. The traditional foundations of the industry are mature, while innovation and higher margins exist in emerging technology applications.

Video Surveillance Continues to Grow

The amount of information contained in high-resolution video imagery is transforming customer expectations and service capabilities, and AI-enhanced features and intelligent analytics are creating new value propositions that customers increasingly demand.

While successful deployments deliver low attrition, high margins, and reduced customer acquisition costs, failures in this space can be costly. The challenge lies in managing massive data volumes – terabytes of high-resolution imagery generated every second – and delivering on promises of AI-driven analysis and automated response capabilities.

The key to success in video lies in realistic expectations and robust implementation. Companies that overpromise video capabilities often encounter problems with false alarms, upset customers, and margin compression. Barnes advised a “fast follower” strategy for integrators, allowing industry leaders to solve technical challenges while following with proven solutions rather than pioneering uncharted territory.

Gradual Integrator Consolidation with Room for Smaller Players

The security industry is experiencing gradual consolidation; however, despite the many headlines, Barnes said it is happening at a slower pace than many expected. Current market structure shows national-scope companies controlling approximately 48% market share when measured by recurring monthly revenue (RMR), with regional players holding 12% and local companies maintaining 23% of the market.

That said, over the past decade, smaller companies’ market share has declined from roughly 50% to 35%, representing a fundamental shift rather than cyclical acquisition activity. Barnes said this change stems from two key factors: larger players like ADT, Vivint, and SimpliSafe have achieved sustainable internal growth rates that exceed industry averages, while many smaller companies struggle to maintain similar growth momentum in an increasingly complex marketplace.

The total number of security companies appears to be declining as smaller players exit the industry, citing increased complexity and difficulty maintaining competitiveness; however, data indicate market share stabilization around 25% for smaller players rather than continued decline to single digits.

Even with the decline in market share, the smaller companies that remain often maintain significant competitive advantages. Wholesale monitoring services enable smaller operators to access monitoring capabilities at costs competitive with the largest direct-to-end-user central stations. More importantly, smaller companies consistently demonstrate superior service delivery and customer retention. Data shows smaller companies maintain lower attrition rates than larger competitors, indicating that personalized service and local market knowledge create meaningful competitive advantages that scale doesn’t easily replicate.

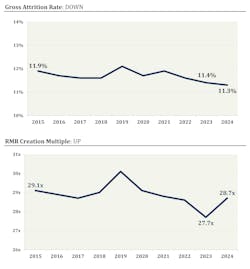

Margin Pressures

Industry operating metrics present a complex picture requiring careful analysis by management teams. Three critical metrics – net margin on monitoring services, customer attrition rates, and net RMR creation multiples – determine overall business value in the industry.

Contrary to expectations that consolidation and scale would improve margins, the industry has experienced declining gross margins on recurring revenues for nearly a decade. Average margins declined from 54% in 2015 to lower levels as alarm companies added smart home services without proportional price increases.

However, Barnes said the past two years have shown encouraging stabilization of margin trends, driven primarily by price increases implemented across the industry in response to inflation and rising costs. Companies that historically implemented modest 1% annual price increases have successfully implemented 3-4% increases with minimal impact on customer retention.

Customer attrition rates have improved steadily since 2019, continuing a positive trend despite the COVID-19 disruption. This improvement reflects both industry growth dynamics – new customers typically have lower attrition rates than seasoned accounts – and operational improvements implemented by companies during the pandemic.

Barnes reported that the underlying reasons for customer cancellations show no concerning trends in either the residential or commercial market segments, with traditional factors like moving remaining the primary drivers. This suggests that service quality improvements and technology enhancements are successfully reducing voluntary cancellations.

The Threats: RMR Creation Costs and Inflation

To Barnes, the most concerning metric is an increase in net RMR creation multiples – the cost to acquire new recurring revenue. After several years of improvement, creation costs increased in 2024, as companies reinvested in growth through increased marketing spending, sales hiring, and competitive pricing.

This increase is particularly problematic because it can offset gains from improved margins and lower attrition. Barnes advised that companies carefully balance growth investments with creation cost discipline to maintain overall value creation.

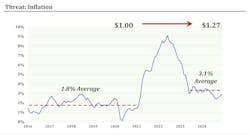

Inflation is another threat facing the industry. Since 2020, general inflation has increased costs by approximately 27%, with security-specific inflation potentially running even higher when considering specialized labor, equipment, and service costs.

Barnes said that most alarm industry executives gained business experience during decades of low inflation and inexpensive capital, leaving them unprepared for the current environment of sustained inflationary pressure. Companies that haven’t implemented 27% price increases over the past five years are experiencing margin compression and reduced returns.

The good news is that customer acceptance of price increases has proven higher than many companies expected. Firms implementing 3-4% annual increases report minimal attrition impact, with some experiencing lower cancellation rates following price increases. This suggests significant pricing power exists in the market due to the essential nature of security services and competitive cost pressures affecting all providers.

Barnes said companies should implement regular price increase programs and overcome historical reluctance to raise prices. The elasticity of demand for security services appears favorable, and customers recognize the value provided. Competitors face identical cost pressures, making industry-wide price increases sustainable.

Failure to keep pace with inflation will result in gradual erosion of profitability and competitive position. Companies must view price increases as essential business operations rather than optional revenue enhancement.

Market Valuation and M&A Activity

Despite economic uncertainties, the market for security company transactions remains robust, with strong valuations across all size segments. Multiple factors support continued transaction activity and attractive pricing for quality companies.

In 2024, approximately 2% of industry RMR changed hands through acquisitions, representing significant but not unprecedented activity levels. Average transaction multiples show clear size premiums – companies with less than $50,000 RMR were averaging 36 times monthly revenue, while companies above $500,000 RMR averaged 46 times monthly revenue.

This size premium reflects scarcity value – fewer large companies exist, creating competitive bidding among acquirers seeking meaningful market positions. The orderly progression of multiples by size indicates a mature, functioning market with rational pricing.

Several factors support continued strong valuations: abundant buyer interest – especially from private equity – available acquisition capital, strong industry fundamentals, and reasonable operating metrics. The combination creates favorable conditions for sellers while maintaining opportunities for strategic and financial buyers.

However, Barnes warned that the market has become more sophisticated in evaluating opportunities. Buyers no longer pay premium multiples simply based on size; they require demonstration of superior performance metrics, growth prospects, and operational capabilities. Companies preparing for eventual sale must invest in financial reporting sophistication and performance measurement.

The correlation between transaction values and internal management sophistication has strengthened significantly. Companies that can articulate their attrition rates, creation multiples, margin trends, and other key performance indicators command higher multiples than better-performing companies that cannot document their results.

Barnes pointed out that this trend emphasizes the importance of investing in financial systems and reporting capabilities, regardless of near-term sale intentions. The discipline required to measure and manage key metrics typically drives improved performance while preparing companies for eventual capital needs or succession planning.

The Takeaways

Barnes reiterated that despite any headwinds, the industry remains in a very strong position, with stout industry fundamentals and growth prospects supporting aggressive business development.

That said, success requires strategic focus and operational discipline. Companies should lean into growth opportunities while maintaining pricing discipline and cost control. The specialty segments driving industry growth require strategic positioning and capability development, particularly around video surveillance and commercial applications.

Most critically, all companies must address pricing strategy and inflation management. Regular price increases have become essential business operations rather than optional revenue enhancement. The window for catch-up pricing may be narrowing as the industry matures and competitive dynamics evolve.

About the Author

Paul Rothman

Editor-in-Chief/Security Business

Paul Rothman is Editor-in-Chief of Security Business magazine (www.securitybusinessmag.com) and has been covering the security industry for various outlets since 2001. Email him your comments and questions at [email protected].