Borrowing From the Bank: David vs. Goliath?

This article originally appeared in the May 2023 issue of Security Business magazine. When sharing, don’t forget to mention Security Business magazine on LinkedIn and @SecBusinessMag on Twitter.

OK…that headline is a shameless bit of click bait. Borrowing from your bank is not – and shouldn’t be – some form of battle, let alone of biblical proportions. Yet, it does involve two parties who have differing views on the money involved, with one of the parties almost certainly being much, much larger.

The average U.S. bank has $4 billion in assets. Prudence suggests that security business owners and executives engage as productively as possible.

The Need

A fundamental aspect of much of the security alarm industry is the need to invest in new customers. On a fully burdened basis (i.e. including all loaded sales and installation and supporting G&A costs), most companies lose money in the creation of new customers and their associated RMR.

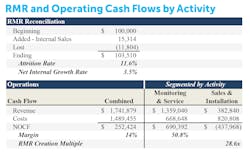

Based on the chart above, on the whole, the company represented generated $1.7m of revenue and $252k of operating free cash flow, with the RMR base growing from $100k to $104k during the year. The segmentation of the results to the right of the chart shows that the company first realized $690k of free cash flow from the monitoring and servicing of the existing customer base (i.e. the RMR and associated billable service revenue) and then “spent” $438k originating $15k of RMR through the sale & installation of new systems.

If the company had no debt and expensed all of its operating costs, the combined $252k of cash flow would also reflect the earnings of the company pre-tax; thus, there is no need to borrow money. But, with every $1 of RMR originated costing $28.60 (the $438k loss in the sales & installation activity divided by the resulting $15k of RMR originated), a quick check of the math indicates that the company would run out of money if it originated $9k more in RMR than it did. So, growth is one reason for looking to access additional capital.

Secondly, if this company was a cross-town competitor you would like to acquire, it might reasonably take something like $3.6m to complete the transaction. There are, of course, a myriad of other circumstances and opportunities that could warrant the need to access capital. A natural question is whether looking to your bank for some or all of this makes sense.

Does Debt Belong in Your Capital Structure?

Debt is typically the cheapest form of capital available, perhaps aside from billing customers in advance. Modern business theory suggests that most companies should have a component of debt in their capital structure, as it allows for higher “leveraged” returns on equity. For example, if a company has $1 million of capital, and it generates $110k of earnings or gain in value in a year, and there is no debt, this provides an 11% return to the $1m in equity.

If the same company has 50% of its capital in the form of debt (i.e. $500k), and it costs $40k in interest (8% – welcome to the world of higher interest rates), then there is $70k left after servicing the debt to go to the $500k of equity, or a 14% return.

Of course, this level of debt is prudent only if there is a highly reliable source of cash flow within the enterprise to service the debt, and marketable assets that provide sufficient collateral. Debt is a fixed obligation, it does not go away just because business slows, or costs increase, so it is appropriate only if similarly fixed sources of cash flow and collateral exist.

When looking at the example company outlined earlier, it is notable that the revenues and free cash flows from the monitoring & service activity are highly reliable, and typically realized through multi-year, automatically renewing contracts with end-users that value the service.

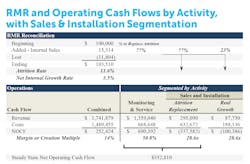

Additionally, the fall-off rate of these customers is usually very predictable, as is the cost that is necessary to originate new RMR to offset this attrition. This results in an annuity like cash flow stream generated by your existing customer base, which is quantified in Figure 2.

This $353k is what we call “steady-state” cash flow (SSCF) – the sustainable cash flow from the existing customer base and subsequent replacement of recurring revenue from customers that were lost. SSCF’s consistency and reliability makes it the perfect source of cash flow for servicing debt. Additionally, the RMR and the enterprise that supports it, have demonstrable market values and can make excellent collateral.

The example company could borrow against its existing RMR, at levels that are easily serviced by the SSCF (with a cushion), and amortized over time, so the debt naturally lowers relative to the SSCF and the RMR. Then, as the company grows its RMR and associated SSCF, these incremental increases can be similarly borrowed against. This provides a rational approach to borrowing, which matches debt to highly reliable cash producing assets.

Rules of the Road

So far, the discussion has been focused on the example company…the “David”. What about the “Goliath?” First, as mentioned earlier, banks are big. This is out of necessity. Their ability to raise capital, and meet increasingly complicated and strict regulation requirements inherently requires size. Secondly, their business model does not accommodate much room for loss. They are looking to lend against reliable cash flows and marketable assets, with lots of cushion.

Loans provide liquidity and greater efficiency in the capital structure. Risk is for the equity (e.g. venture capital, private equity, entrepreneurs etc.).

This is why your bank can offer the lowest cost for the capital. One of the biggest mistakes we see are potential borrowers who communicate to a lender that their opportunity is low-risk. From the bank’s perspective, they want to see no risk.

The combination of size and risk aversion leads to standardization. They prefer their loans to fit into tidy boxes.

Here are 5 things a security business owner or executive needs to do in order to be a compelling borrower:

1. Articulate your company’s performance along the lines shown above and do this over a multi-year period in order to establish trends and identify areas of operating volatility. If needed, a financial partner like us can help. (see the contact details at the conclusion of this article).

If, for example, your attrition rate bounces around periodically, take this into account and do not seek to borrow under the assumption it will remain flat. Do this analysis based on your financial results on a cash basis. Accounting convention may, for instance, allow you to capitalize some costs, but these costs are real and require capital – even if they can be put up on a balance sheet and written off over time.

The nature and vagaries of this industry’s operating dynamic and accounting can be highly confusing and distorting of results. It is best to talk with your bank about your business on a cash basis, and then help them see how your accounting policies are applied.

2. Think belt and suspenders. The bank needs to see both the reliable source of cash flows that will service the debt, and the value of the assets that will collateralize the loan. You need both.

3. Get your financial statements audited by an accounting firm, or at least reviewed. Yes, it is expensive but worth it when seeking to borrow. There is nothing worse than being rejected for a loan solely due to not having three years of audited financials. Compelling analysis in the first point above will only carry water if the underlying numbers have been independently verified.

4. Understand the need for cushion. The bank will require it. They may only want to lend up to 60% of the value of the assets, and/or have the highly reliable cash flows equal at least 1.3x the amount of debt service plus any other fixed obligations.

There is no bank that will allow you to borrow 100% of the value of the assets or lend an amount that will require 100% of your cash flows to service; and if you find one, do not borrow from them. Remember, you want cushion as well. As a secured lender at the top of the capital stack, the bank will have rights that could foreclose on your business or require additional equity investment if you do not perform. Be conservative.

5. Be professional. The bank will want to underwrite your character, discipline, and ability to manage your enterprise. They are looking for a team, and a steady hand that knows what it is doing. They want an enterprise that is up to the challenge of providing the services associated with the RMR contracts 24/7/365. Save the hard charging, high-flying entrepreneurship for your equity investors.

Hedge Your Bet

It is important to develop relationships with other lenders – even if your current bank is meeting all of your needs, and you have dealt with them for years.

The banking industry is consolidating and changing, just like the security alarm industry. They are large organizations and are capable of sweeping changes that can hugely impact your business. In the last several years, a couple of banks that had routinely and skillfully lent to the industry decided to stop doing so. It was highly disruptive to many. Additionally, they can fail. Ask the borrowers from Silicon Valley Bank (check out www.securityinfowatch.com/53028465).

The best strategy is to stay plugged into what is happening in the industry, go to trade shows, belong to your trade association (such as ESA) and share thoughts with other members, and talk to experts like us. Be in the flow and develop options, which will help make sure you are not accidentally stepped on by a giant.

Michael Barnes ([email protected]) is President of Barnes Associates Inc., a brokerage, advisory, and consulting firm specializing in the security alarm industry. His firm also co-sponsors the annual Barnes-Buchanan Conference (www.barnesbuchanan.com). Joe Thompson ([email protected]) is Senior VP of Capital Markets for Barnes Associates.

About the Author

Michael Barnes

Michael Barnes

Joe Thompson

Joe Thompson ([email protected]) is Senior VP of Capital Markets for Barnes Associates.