The Smart Money: How Smart Homes Are Reshaping the Insurance Industry

This article originally appeared in the January 2024 issue of Security Business magazine. Don’t forget to mention Security Business magazine on LinkedIn and @SecBusinessMag on Twitter if you share it.

The smart home sector is poised to significantly transform the conventional home insurance industry. This evolution will enable the utilization of new data to develop innovative services and revenue streams, thereby altering how insurance providers interact with consumers. This shift presents considerable obstacles to the insurance industry's established data-centric models.

In the era of the Internet of Things (IoT), an influx of data from interconnected devices is imminent. Insurance companies, seeking the most profound insights, must find ways to access this data directly. Traditional methods of data collection via third parties may become obsolete, as IoT data emerges as a crucial competitive asset that companies are unlikely to share freely. Control over customer relationships and data utilization will likely shift to the entities implementing smart home technologies, who can then offer their customers enhanced services that improve home safety, energy efficiency, and manageability.

As the smart home market continues its steady growth, stakeholders actively seek to enhance value. According to Parks Associates research, 42% of U.S. households have at least one smart home device, and the highest adopted device is the video doorbell – now in 20% of U.S. internet households.

Currently, only 10% of households own a smart smoke/CO detector, and only 3% own a smart water leak detector. Water-related damage is by far the most common home damage experience reported by consumers. The average cost of water damage/leaks is $9,633 and $8,625 for flood/weather-related damage, according to the Insurance Information Institute.

Integrating insurance products into the mix is a compelling strategy. Such integration poses a challenge to traditional insurance models and may marginalize existing carriers’ however, this also presents an opportunity for insurers to adapt by incorporating smart home technologies into their primary offerings and actively participating in this new market.

This approach could lead to new avenues for revenue generation and catalyze a fundamental shift, with insurance carriers transitioning from a reactive stance – merely providing coverage against losses – to a proactive role in preventing such losses.

The Security Market Jumps in

The security system is a major avenue for the adoption of smart home devices. Extending peace of mind with smart home security and safety solutions taps into the same sense of peace of mind provided by property and casualty insurance. Both aim to promote a feeling of being safe or protected.

While security and smart home providers have pursued insurers as a channel for smart home products, very few insurers sell or distribute smart home monitoring systems or devices today. Instead, insurers are making smart partnerships that can drive new sign-ups and smart home tech through incentives.

State Farm’s $1.2 billion investment in ADT sets an example, prompting other insurers to take the smart home space seriously. These partnerships can boost market presence and bolster ADT's growth. Overall, these alliances improve preventive measures for insurers and policyholders.

Additionally, Goosehead Insurance has partnered with Vivint Smart Home to develop a combined smart home and insurance solution, and Goosehead also acquired Vivint Insurance Agency's business. Startups Hippo and Lemonade continue to push the industry to innovate, with Lemonade expanding into auto insurance and Hippo offering discounts on an expanding number of smart home tech, including devices from Ring, Simplisafe, Kangaroo, and Notion.

These collaborations enable insurers to reduce risks, enhance customer engagement, differentiate themselves in the market, and tap into the growing smart home technology sector. It's a win-win strategy that benefits both the insurance industry and homeowners seeking enhanced protection and peace of mind.

The Opportunity for Insurers

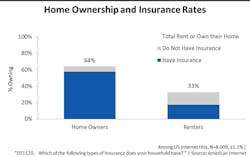

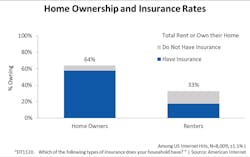

In Parks Associates’ Q2 2023 survey of 8,000 internet households, 64% were homeowners and 58% reported having a homeowner’s insurance policy. Overall, roughly 90 million U.S. internet households have a homeowners or renters insurance policy. Homeowners are the larger market, and insurance uptake is far higher among homeowners than renters.

The integration of smart home technologies presents a significant opportunity for insurers to innovate beyond their traditional business models.

Insurance companies are increasingly interested in smart home device data because it allows them to better understand and manage risks, offer personalized policies, reduce losses, engage with customers more effectively, and gain a competitive edge in the market.

The integration of smart home technologies presents a significant opportunity for insurers to innovate beyond their traditional business models. This evolution aligns closely with consumer motivations for adopting smart home systems, providing a promising avenue for an industry that has seen minimal change over three centuries.

While technology has refined insurers' business processes, the core of their success still hinges on sophisticated pricing algorithms that rely on conventional data sets. Furthermore, the transactional essence of insurance has remained stagnant, with annual customer interactions focused primarily on price, leading to a purchase of a product both parties hope remains unused. This scenario offers little in the way of genuine consumer engagement.

Smart home technology disrupts this status quo by fostering a collaborative relationship between consumers and insurers, centered around safeguarding what is most valuable: the home and family. This technology serves as a catalyst for an array of new services, potentially elevating insurance companies to the role of a “home concierge.” Such a role encompasses a range of value-added services connected via a digital platform – for example, a smart home system could automatically notify a plumber in the event of a water leak, or issue seasonal reminders for home maintenance tasks.

More Security Partnerships to Come

In this evolving landscape, security players will be pivotal business partners. Their role in designing and managing smart home systems places them at the forefront of this shift, offering unique insights and control over the data stream.

This positions them as key allies for insurance companies looking to integrate these technologies into their services. By collaborating with security firms, insurers can access real-time data that enhances risk assessment, enables proactive loss prevention, and customizes insurance offerings based on individual household needs.

This partnership can lead to more dynamic and flexible insurance models, where premiums are adjusted based on actual usage patterns and risk profiles. Additionally, insurers can leverage these partnerships to offer bundled services, combining insurance with home security solutions.

This not only enhances the value proposition for customers but also opens new revenue streams for insurers, diversifying their business models in the process. This shift represents a significant leap from traditional insurance practices, heralding a new era of consumer-centric, technology-driven insurance solutions.

Elizabeth Parks is President and CMO of market research and consulting firm Parks Associates. Its report, Insurance Opportunities in the Smart Home, investigates consumer preferences for IoT devices that can impact insurance premiums or claims and evaluates the opportunity for IoT growth through the insurance channel.

About the Author

Elizabeth Parks

Elizabeth Parks is the President of market research firm Parks Associates. For more information, visit www.parksassociates.com