The Smart Money: Residential Smart Video Hits the Next Phase of Growth

Key Highlights

- Smart video is the dominant smart home category with 33% U.S. household penetration and nearly 30 million annual unit sales projected by 2030 — but hardware is commoditizing fast, and the real competition is shifting to AI, subscriptions, and ecosystem control.

- With 76% of smart video owners paying for related services and subscription prices rising, the business model is increasingly recurring-revenue-driven — but alert quality is the loyalty linchpin, with Net Promoter Scores swinging 20-30 points based on whether alerts are relevant or just noise.

- The integrator opportunity is real: pro installation drives measurably higher satisfaction, 86% of buyers want bundled smart home devices, and whoever controls the intelligence layer and subscription relationship will own the customer long-term.

This article originally appeared in the March 2026 issue of Security Business magazine. Don’t forget to mention Security Business magazine on LinkedIn or our other social handles if you share it.

Smart video products have secured their position as the leading category in the smart home market, anchoring both device adoption and recurring service revenue; however, as the category matures, competitive dynamics are shifting rapidly.

Hardware expansion, AI-driven differentiation, subscription monetization, and ecosystem alignment are redefining how value is created and sustained. The next phase of growth will be determined less by camera specifications and more by intelligent services, interoperability, and long-term customer relationships.

Editor's Note: Parks Associates analyst Jennifer Kent first examined this market in our January 2026 issue; here, company president and CMO Elizabeth Parks goes deeper on the business implications.

Adoption Leadership with Room to Grow

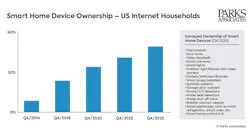

Smart video devices – including video doorbells, smart cameras, and floodlight cameras – are now the most widely adopted smart home products after smart speakers and displays. Parks Associates research shows 33% of U.S. Internet households report owning at least one smart video product, underscoring the category’s mainstream penetration. Multi-device households average 2.2 cameras per home, signaling engagement and expanded opportunities for service attachment.

Demand remains resilient despite broader economic pressures. Nearly 25 million smart video units are projected to sell in the U.S. in 2025, increasing to more than 30 million units annually by 2030. By the end of the decade, annual unit sales revenue will reach $4.5 billion. This sustained growth reflects the category’s central role in delivering peace of mind, property protection, and convenient access management: core pillars of the connected home value proposition.

Hardware Commoditization Accelerates

As the installed base expands, competitive pressure is intensifying. Nearly every major vendor has broadened its portfolio across indoor, outdoor, floodlight, pan/tilt, battery-powered, solar, and ultra-budget models. Resolution upgrades, enhanced night vision, and flexible power options are now table stakes.

Smart cameras increasingly anchor broader device bundles, with 86% of purchasers interested in bundling video products with other smart home devices.

The result is a market increasingly defined by coverage breadth rather than singular hero products. Brands seek to occupy every price tier and installation scenario to retain customers within their ecosystem. While this strategy protects share, it also accelerates hardware commoditization. Differentiation based solely on device specifications is narrowing, compressing margins, and elevating the importance of services and software innovation.

AI Becomes the Core Differentiator

Artificial intelligence has moved from incremental enhancement to primary value driver. Vendors are positioning AI capabilities, such as object classification, pet tracking, descriptive alerts, blind-spot monitoring, and proactive deterrence behaviors as central selling points. Cameras are evolving from passive recording devices into active security participants capable of interpreting and responding to events.

Consumers demonstrate strong interest in these capabilities. Theft alerts and advanced analytics that improve alert relevance rank highly. Notably, 57% express interest in AI systems that proactively engage with visitors to assess intent or deter unwanted activity. This shift reflects rising expectations: users no longer want footage alone – they want meaningful interpretation and action.

In this environment, AI sophistication, contextual awareness, and automation integration become primary levers for differentiation. Hardware provides the sensor layer; intelligence defines the experience.

Recurring Services Define the Economics

The smart video business model is increasingly subscription-driven, with 76% of smart video device owners paying for a related service, whether bundled within a professionally monitored security system or attached to a stand-alone video product. Standalone video services now account for one-quarter of the home security services market.

Video doorbells are particularly effective at attaching paid services, achieving a 66% attach rate. Outdoor camera owners also demonstrate stronger subscription uptake compared to indoor-only owners, reflecting a greater need for storage and event review.

Cloud storage dominates usage patterns, with average monthly spend reaching $11-13 across categories. Leading brands have raised subscription prices and introduced premium tiers offering 24/7 recording, advanced AI analytics, and enhanced deterrence features. Consumers are increasingly conditioned to view camera ownership as an ongoing service relationship rather than a one-time purchase.

At the same time, hybrid and local-first models present opportunities. As device sunsets and subscription fatigue erode trust, local storage options combined with optional cloud enhancements can address privacy concerns and appeal to cost-sensitive households. Providers that balance recurring revenue growth with transparency and long-term product functionality will be better positioned to sustain loyalty.

Alert Quality Drives Loyalty

Alerts are the daily touchpoint between users and their video systems. Most receive alerts daily, and the vast majority consider them timely and actionable; however, dissatisfaction remains significant: 37% cite false triggers, and 36% report excessive notifications.

Alert relevance has a measurable impact on brand advocacy. When alerts are helpful, Net Promoter Scores reach the 60s; when quality declines, scores fall into the 30s or 40s. The implications are clear. Precision filtering, contextual understanding, and adaptive personalization are foundational to retention and service stability.

Improving alert intelligence represents one of the most direct pathways to reducing churn, increasing subscription stickiness, and strengthening ecosystem lock-in.

The Evolving Buyer Journey

E-commerce is the dominant purchase channel, with more than half of smart camera and video doorbell buyers purchasing online; however, professional installation services are gaining traction. Users who choose pro installation report significantly higher satisfaction levels.

This dynamic presents an opportunity across the value chain. Manufacturers and retailers must optimize digital storefronts, while security providers and service-oriented players can differentiate through installation expertise that ensures optimal camera alignment, network configuration, and feature utilization.

Additionally, smart cameras increasingly anchor broader device bundles. Eighty-six percent of purchase intenders express interest in bundling video products with other smart home devices. Motion sensors lead desired bundle components, followed by smart door locks, lighting, additional cameras, dash cams, smoke/CO monitors, and thermostats.

Interest in traditional wall-mounted security panels is limited (15%), signaling a consumer-driven redefinition of what constitutes a “security system.” Consumers prefer modular, app-centered ecosystems that combine awareness, automation, and access control without legacy hardware constraints.

Notably, one in five video device intenders expresses interest in bundling a dash cam, pointing to expansion opportunities that extend video monitoring beyond the home.

Ecosystem Competition Intensifies

Smart video increasingly operates within broader automation and platform ecosystems. Some brands integrate with larger platforms rather than managing their own end-to-end environments, leveraging solutions such as Apple HomeKit Secure Video or Google Home-powered devices. The introduction of Matter 1.5 with camera support raises strategic stakes around customer ownership and experience centralization.

As interoperability improves, competitive positioning will hinge on who controls the intelligence layer, data insights, and subscription relationships. Ecosystem partnerships expand reach but may dilute direct customer ownership. Strategic alignment decisions made today will shape long-term monetization potential.

Editor’s Note: This data comes from Parks Associates’ latest study, Smart Video Products: Business Models & Features. Join the firm at the 30th annual CONNECTIONS Conference, May 5-7, in Santa Clara, CA. www.parksassociates.com | www.connectionsus.com

About the Author

Elizabeth Parks

Elizabeth Parks is the President of market research firm Parks Associates. For more information, visit www.parksassociates.com